hedge-fund.io

Snippets

|

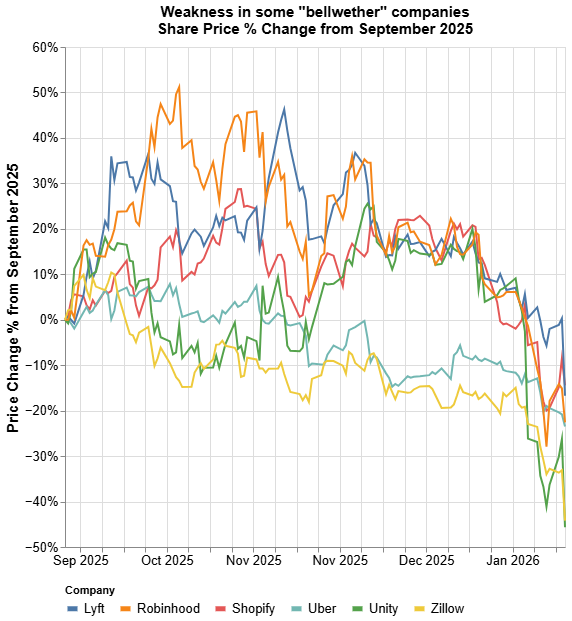

Snippets are works in progress and so ask questions rather than attempt to provide answers (yet). UK homebuilders most shorted by hedge funds - 15 July 2026

1Short interest data from FCA

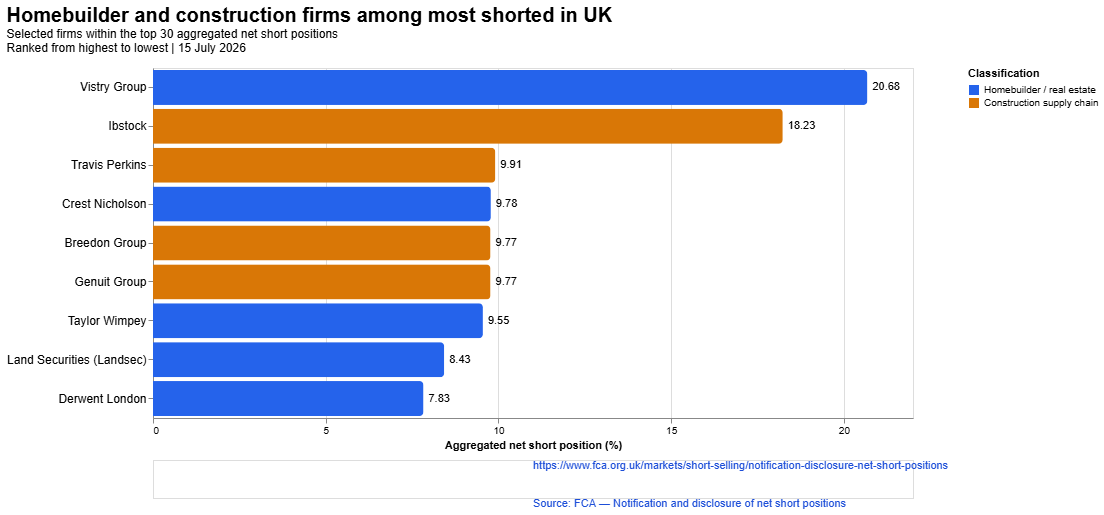

Disclosure: We recently increased our long positions in various UK homebuilders. Not financial advice. Do your own due diligence and research. FCA Changes Short Reporting Rules The FCA changed their reporting process for declaring short positions. They no longer list individual funds behind short positions and they have lowered the reporting (or publishing) threshold from 0.5% to 0.2%. The net effect of which is that we can no longer produce the granular chart from the previous short disclosure. On the other hand, it reveals a closer approximation to the true short position - for example showing a 20% of float aggregate short position in Vistry PLC. UK Homebuilders have a large instituitonal ownership base Depending on which source you consult, 60-90% of shares of Vistry are held by institutional investors. With a market cap of £841m, of which nearly £170m is shorted only about 10-40% (£84m - £320m) of shares aren’t in institutional hands. Much of this is also held by mutual funds and ETFs which might not necessarily sell off shares soon, especially if they’re carrying an unrealised loss. So if there’s a sudden surge in buying, on the back of a headline or the announcement of more detail of the “biggest council house building programme since the postwar era”, or further falls in gilt yields (all of these are MAJOR ifs), we wonder whether a “short squeeze” might occur - a rush to cover short positions opened or deepened at already all-time-low levels. Dear Andy Burnham: Build More Houses We think more houses should be built in the UK, of various sorts - council houses, mansions, and multi-family residential blocks and skyscrapers alike. Perhaps homebuilders need reform and perhaps they need to fail or reach death’s door, at which point the government may rescue them and wipe out equity holders’ positions (such as ours). But perhaps they need more money, a supportive regulatory environment, and a charismatic champion in No10. And perhaps a bit of a scathing, even shaming media campaign targeted at international hedge fund giants with balance sheets in the billions, bleeding out what remains of a sputtering homebuilder sector. Shorting is not inherently bad Make no mistake - we support activist investing and that includes shorting at times.. And if a hedge fund sees a company being poorly run, perhaps shorting it is both the prudent and moral thing to do. But if a problematic environment - whether because of funding, market or regulatory conditions - is weighing on a company, then perhaps shorting it into oblivion, rendering its workforce unemployed, and ultimately hamstringing its ability to take risks or to hire talented people - perhaps then shorting no longer has the moral highground. Barratt Redrow announced a £400m stock buyback, instead of paying out dividends today. Its stock was up only about 4% today. Crest Nicholson, which reports earnings tomorrow, was up around 10%. A handful of homebuilders are up around 20% since the mid-June lows. We’ve seen this before. It is very likely the case that this is one of the last upticks in a secular stagnation that ends in bankruptcy or restructuring on a sector wide level, perhaps even providing the new Prime Minister with a platform to support nationalisation or reform of these companies. We hope not today. We hope funding conditions ease and that the new leadership puts its money where its mouth is, and builds some more houses. Ultiamtely investing is about providing capital to organisations to take risk on your behalf, and to provide value to society. Building houses is perhaps one of the most beneficial of these. Just be sure to build them where people actually want to live. Who is Short UK PLC and What if Burnham is Good for Real Estate? - 25 June 2026

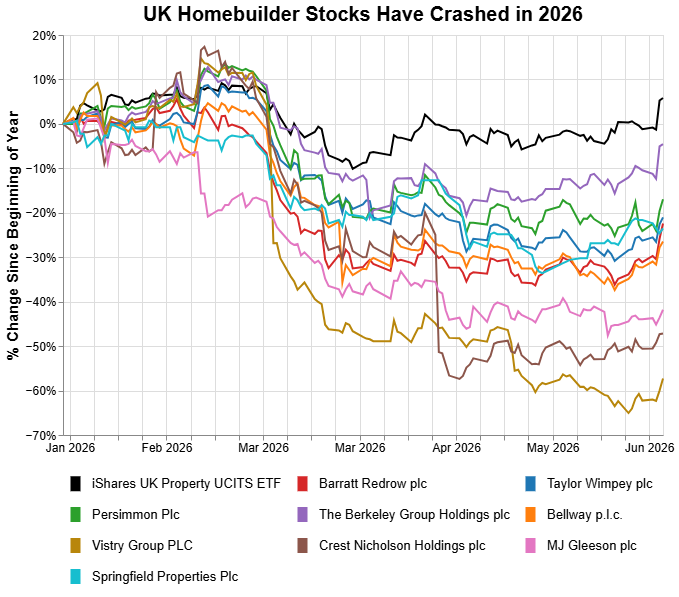

1Short interest data fromFCA We find ourselves interested again in the bloodsport of catching falling knives - more specifically, which UK companies have performed poorly, are currently most “shorted” (according to the FCA) and could have near-term triggers for a turnaround? A somewhat embarrassing declaration: we own Ocado, Wizz Air, Ibstock and Vistry Group and some other homebuilders. Suffice to say national pride has not served us well here. Segro rejected a £12.6 billion takeover offer from Prologis and still saw its share price climb with nearly 20% yesterday. This helped to put the MSCI UK Property ETF up over 6.6%, its 3rd best day in 5 years (topped only by the March 2020 Covid meltdown recovery, and a spike in 2023). We also noted that a handful of deeply beleaguered UK homebuilders (Vistry, Barratt, Berkeley, etc) were up a few % points today and seem to have recovered from their lows in mid-June. Now a single such data point does not a pattern make - but could it be the start of something more? What would it take to bring the hyperscaler playbook (vendor financing or cross-ownership investment deals) to the UK homebuilder industry? We could not help but notice that this performance aligns quite well with the surge in Andy Burnham’s odds on Polymarket of becoming the next UK Prime Minister (and incidentally with falling gilt yields). Burnham’s Manchesterism could well see more of the booming development which he championed in Manchester, and seemingly quite actively supported with his approval of loans to Daren Whitaker’s Renaker. He is already outlining plans for devolution, with intentions to set up a “Number 10 in the north”, with powers over some areas like skills and taxes being delegated to regional bodies. UK Homebuilders We won’t go so far as to say Burnham’s election as prime minister is going to spur a homebuilding renaissance that will lift these sputtering British stocks back to their multi-billion pound former glories (one can dream). But we would not be surprised if a kind of “buy the rumour” trade emerged - that Burnham might be good for the prospects of real estate developers. Because Burnham has certainly proved that people can make a lot of money through building real estate development. And it’s far more noble, we think, to make money from building lots of houses (whether they’re affordable/social housing or luxury highrises - ideally both) than from just sitting on houses which appreciate because of supply constraints.

1Stock data fromYahoo! Finance A Decent Proposal We believe homebuilding in the UK will happen when the correct incentives are in place. Cynically, we think that means when both political incumbents and the constituents they serve stand to benefit more from increasing the housing supply, than from merely keeping it as restricted as possible. In light of these we (somewhat tongue in cheek) propose the following ideas to facilitate that:

Could Diamonds be AI’s best friend? - 4 June 2026

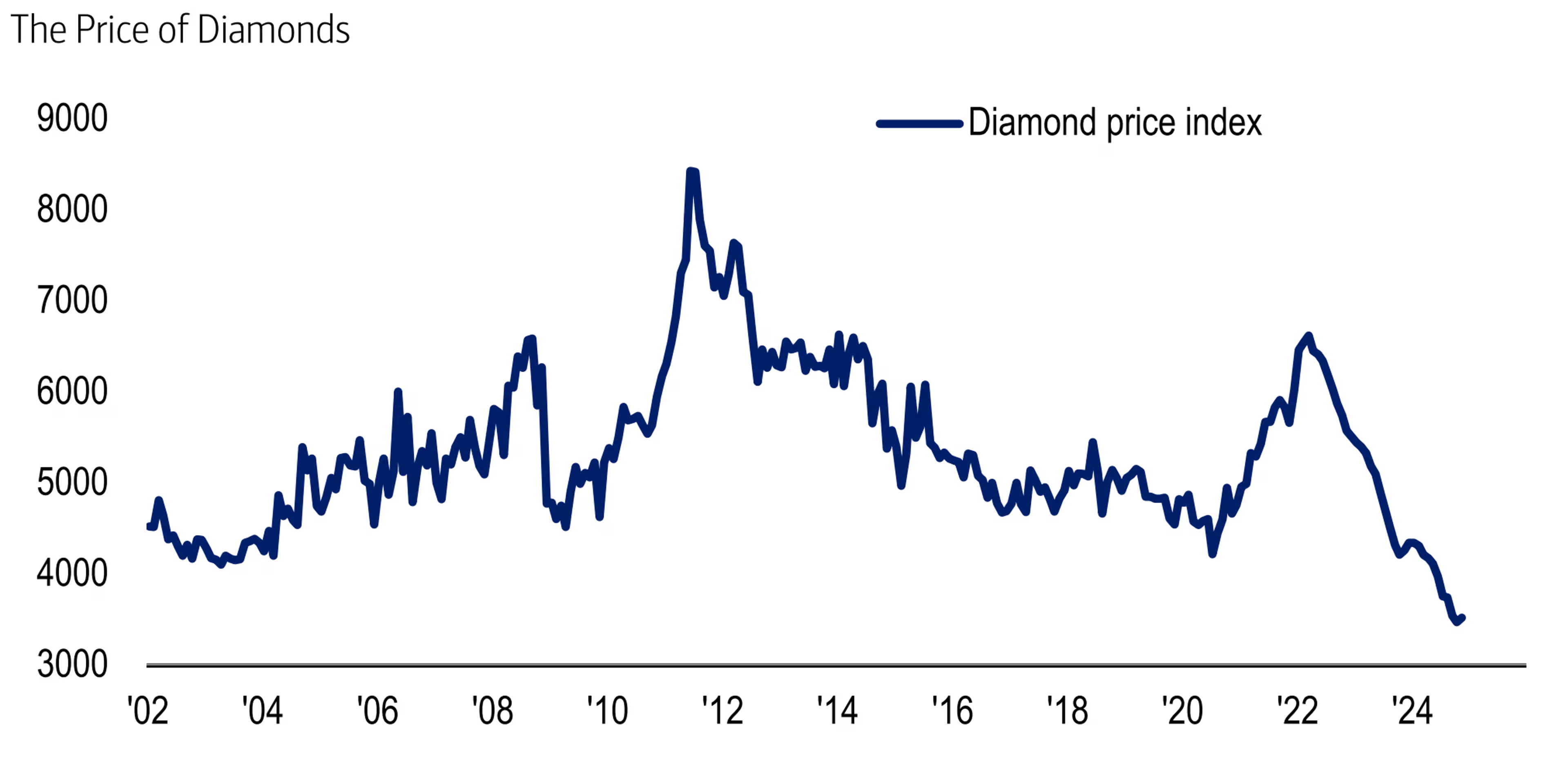

1Image from BofA via The Guardian When you walk out of Bond Street station there is a massive De Beers billboard. Known for their iconic "A Diamond is Forever" marketing campaign, their marketing has seemed absent in recent years while a collapse and consolidation has taken place in the natural and lab grown diamond industry. In October 2025 they announced their largest category marketing investment in a decade around Desert Diamonds and have followed up this week with further promotion. And there appears to be the faintest hint that diamond index prices are stabilising after a precipitous decline since 2022 to record lows. The record lows also drew the attention of Apollo’s Torsten Slok. We think something is happening. The perfect storm which has led to these price declines (over supply of both natural and synthetic diamonds ) may be starting to reverse - tightening of supply, increased industrial demand for synthetic diamonds, and a renewed marketing push from De Beers potentially driving natural demand. Cooling transistors with diamonds A recent Bloomberg article highlighted the sharp rise in stock prices of Chinese companies related to the use of synthetic diamonds in new chip-cooling applications. In October last year a Stanford research group published findings on how they managed to grow polycrystalline diamond at low temperatures and through integration with gallium nitride transistors significantly lowering device temperature. Investing in “AI supply chain” stocks have become something of a meme in recent weeks, particularly following the release of Dylan’s AI bottlenecks app and caution is certainly warranted. However there is potentially an investment narrative here. If lab-grown diamond production capacity gets shifted to this cooling use case perhaps the sputtering diamond mining sector may be due for a revival. Diamonds have also been used for high bandwidth non-volatile storage as highlighted in this recent (2026) paper published in Carbon journal. Stabilisation in Lab-grown diamond prices Wholesale prices for lab grown diamonds appear to be stabilising, after having fallen over 90% since 2018, based on the Lab Grown Diamond index from Edahn Golan. Q4 saw the smallest quarterly decline in prices since the introduction of the index, around 5%. Costs for high-pressure high-temperature lab grown diamonds have started to increase as Chinese HPHT factories collectively ceased price cutting. The 2025 BriteCo report highlights that nearly half of engagement rings purchased in the US contained lab grown diamonds and that significant price disparity persisted with a 1-carat lab grown diamond averaging $1000 compared to around $4200 for the natural equivalent. Perhaps we will see some of Jevon’s Paradox here - in that as prices have declined, overall demand for the resources may increase as it becomes more accessible to a wider range of buyers. Average carat sizes for lab grown rings have nearly doubled since 2019. If synthetic diamond prices rise, and with it the jewellery that contains them, this could spur price increases for natural diamond jewellery as well. Contraction in Natural Diamond Supply Diamond output in the world’s second largest extractor is being constrained. Botswana is sitting on a diamond stockpile of double its targeted inventory level. Low prices brought on by weak global demand and the proliferation of lab grown diamonds have forced the Debswana joint venture with De Beers to temporarily suspend some mines’ production last year. In 2024 Botswana produced 18 million carats of diamonds, second only to Russia. Alrosa, the world’s largest diamond producer, accounts for more than a quarter of the world’s diamond extraction despite having been sanctioned by the US and the EU in recent years. In addition to these sanctions, Russia is now also considering imposing export duties on some rough diamonds. Verdict We have seen a certain price cycle repeat over and over:

The extent to which this process will repeat for diamonds remains to be seen, and the extent to which an investor can capitalise on this is also not entirely clear - listed diamond mining companies could be on their last legs and may very well fail or become acquisition targets by larger players before (if ever) their share prices recover. It is fraught with risk. But their depressed share prices could present an asymmetric opportunity - we think it might be worth a position. We’ve allocated some capital to a handful of listed diamond mining names and still hold a small position in Anglo American. DiamondFloor - A Marketing Proposal As part of this investigation we also propose the idea of a DiamondFloor: a marketing entity, vertically integrated and owned by the mining company, which sets a minimum floor price guarantee for the price of the stone which is inline with the final consumer price of the diamond. This can initially be limited to specific stones of exceptional quality and size and, in order to highlight the superiority of natural diamonds, this can be integrated with blockchain provenance/origin services like Tracr which DeBeers has been developing since 2018 and which the GIA recently took a 30% stake in. Historically diamond jewellery has had significantly reduced resale value, partly because of overheads that retail distributors (shops) have to cover. But if the retail shop is sufficiently vertically integrated and if ancillary costs are a sufficiently small percentage of the total cost of the jewellery, they could potentially offer a price floor without jeopardising their profits, while maintaining a “guarantee” of value for a premium, exceptional, rare item. After all - how many people will really return a high-end piece of jewellery? And if one’s business model cannot withstand that risk, are you really in a sustainable and truly value-adding business? Perhaps for this to work diamond producers would first need to turn the tide of decreasing prices. Perhaps that has already happened. The State of AI Part 3: Token-minning - 27 May 2026Demand for compute has been driving the demand for GPUs and with it the demand for memory, CPUs and perhaps the entirety of the AI trade. Token-usage underpins compute demand and various market participants see token-usage growth continuing on its recent parabolic trajectory. However past results do not guarantee future returns - there is no guarantee of this growth. Scenarios that could, in the very near term, begin to weigh heavily on this token-demand:

The Continued Rise of Local Adam Conway, XDA’s lead technical editor, recently shared his experience of using a locally run LLM to replace ChatGPT for various uses. Running Alibaba Qwen-3.6-27B on his Radeon 7900 XTX he was able to perform a number of tasks that he’d normally use ChatGPT for. That model beats the previous generation Qwen3.5-397B-A17B MoE on SWE-bench verified - an impressive feat to say the least. It also performed well on vulnerability detection. And adding the coding agent Pi to it rounds off the experience. Electricity usage was also entirely reasonable. It will be interesting to see whether this story gets repeated and more people start entirely relying on local models for most of their AI queries. Technical Innovations at the Frontier Brandon Carl highlights the following reasons for the “end of the resource exponential”:

It is no secret that a wave of AI startups are looking into the question of how to make models more efficient. We expect these sorts of companies to proliferate. We wonder however whether the hyperscalers will simply invest in or acquire these sorts of companies which could slow down the impact of their findings. Token-Maxxing Backlash continues

Uber COO Andrew Macdonald is the latest prominent business figure to come out against significant spending on AI without a clear way to measure the impact it is having. This follows earlier statements in April by Uber CTO Praveen Naga that Uber had by then already exhausted its 2026 Claude Code budget. Microsoft recently also mentioned that the company had started cancelling Claude licenses after token budgets were overrun and instead many developers will use Github’s Copilot CLI instead. Token-maxxing.io highlights a handful of other companies that have appeared in the news recently in articles on that topic. It should not come as a surprise that this phenomenon will likely be used as a justification to increase the resolution of scrutiny over AI use in companies, which will likely include more itemised monitoring and productivity assessments of employees as well. Aiswarya Sanker of EntelligenceAI’s Twitter post that of each $1 total AI spend, 44% is lost on bug fixes and only 18% reach users, has already received over 1m views in a day. Ultimately there appear to be significant forces already in play driving towards more efficient token-usage - by enterprises and by models alike. It remains to be seen whether overall token-usage continues to grow quickly enough, and models become more efficient, to outrun the enterprise backlash that appears to already be unfolding. More heat and power cuts in London - 26 May 2026

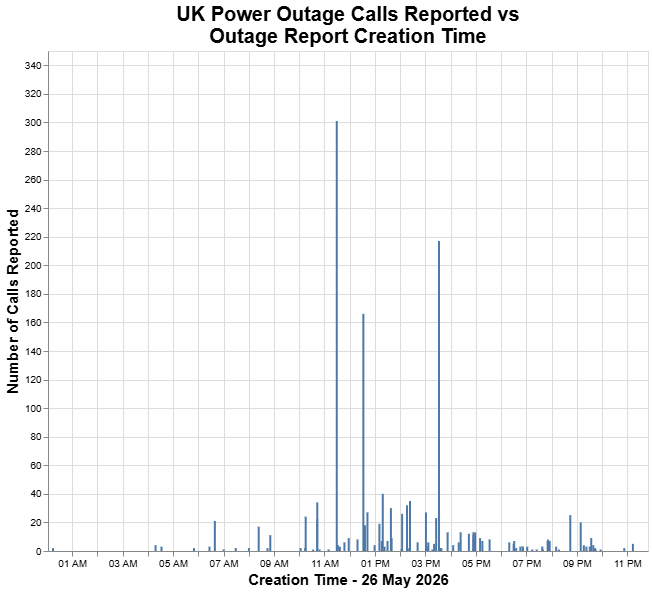

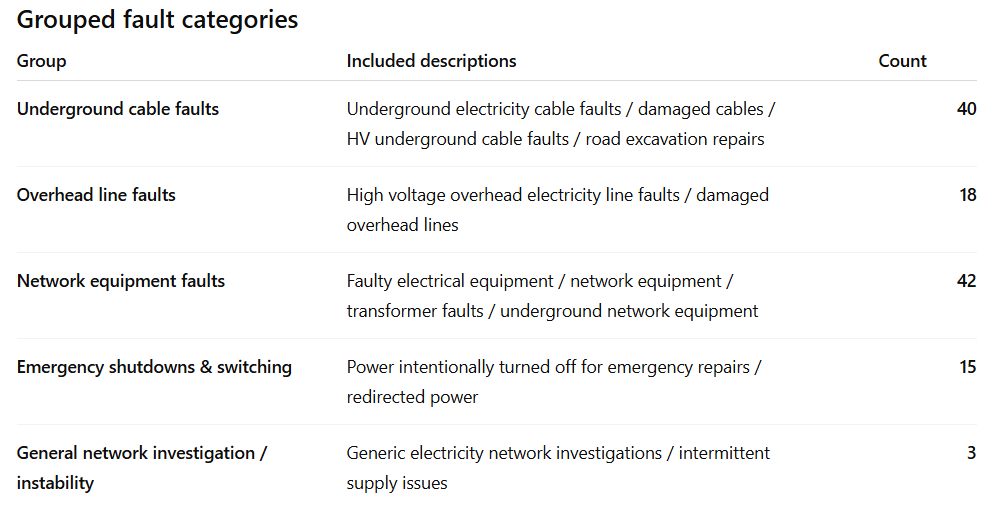

1Power cut data from UK Power Networks London broke its May temperature record for a second day in a row, reaching 35C. Incidentally, a tall building in central London was again part of an unfortunate urban block that suffered a power outage, and so additionally was without power, water, lift service and for a major broadband provider, without internet as well. Today however there were three cuts throughout the day affecting that specific postcode. And at one point in the day there were over 180 incidents (planned, unplanned or restored outages) listed on UK Power Networks. It is not immediately clear whether there is historical data or some other historical API feed available for the Live Outages but it would certainly be interesting to compare number of outages over different days, and also whether the heat had an impact. Of the “unplanned” and “restored” outages, they fell into the following broad categories, with “underground cable fault” and “network equipment faults” dominating.

We wonder again whether the heat, or the power demand from e.g. airconditioning triggered these faults and if so whether any grid improvement or broader resilience planning will be forthcoming. We will certainly be monitoring that data source. London - Overheating in a Blackout - 25 May 2026The UK had its hottest May day on record today, with Kew Gardens hitting 34.8C. Incidentally on this day there were a few power outages in London, potentially unrelated. One of these outages affected a tall residential building in the City of London. This shut down the lifts. This also shut down the water for the higher floors. And shortly after that a large broadband provider reported an outage incident in that vicinity as well. In an instant, at least 50, perhaps 100, people in that building were suddenly without water, electricity, internet connectivity (excluding cell phones), unable to easily leave or return to their property and that in temperatures above 30C. The initial reaction to this is perhaps “first world problems!” But this is late May. Not July, which is the month that saw 40C in several places in the UK in 2022. The reality is that this is still a thing that the UK, in particular London, is woefully underequipped for. We wrote about the substation fire (sabotage) in Berlin in January this year that affected nearly 100 000 people and saw temporary accommodation set up for people because their heating was also affected. At least it’s not freezing at the moment. And of course, this heatwave may very well blow over so that the country can be enveloped in the mild, cloudy, drizzly 50 shades of grey that often passes for British Summer… But what if it doesn’t? What if London breaks 35C or even 40C again this year, and does so several times? For days on end? With so many people still working from home in the UK, particularly in London, an unusually hot summer could see a significant increase in airconditioning power consumption. In addition to the ongoing pressures of aging grid infrastructure, increased electric vehicle usage, electrified heat pumps, renewable intermittency, the additional electricity consumption from residential airconditioning going fully mainstream might just push the grid beyond its limits this year. What then? One need only look at the case of South Africa - a case study like no other, in which rolling blackouts caused by poor planning, maintenance and frequent sabotage, spurred huge residential investment in solar PV backup power systems. Of course the UK is notoriously not nearly as sunny as South Africa so blackouts might not lead to a massive solar deployment but it is a very quickly deployable decentralised power source. But such blackouts could foreseeably increase demand in the following sectors:

If you are suddenly without water, electricity or connectivity at home, for an extended period of time even if intermittent, then your first port of call would likely be the office or coworking space that might be able to provide economies of scale alternatives where individual cost is too high or impractical. We are conscious this resembles a bit our “end of the world” basket which we looked at early in January. And which, ironically, has probably significantly outperformed our actual portfolio. We wonder whether derivatives on solar panels or used EV batteries might be a useful financial instrument. It should not come as a surprise that the organisations best prepared for utility (energy, water, communication) disruption include the hyperscalers. Vast data centers that host high-fidelity abstractions of the entirety of human knowledge, increasingly powered by on-site power generation, satellite communications technology (at least in the case of SpaceX/XAi and of Amazon with its Blue Origin and Kuiper plays) - these behemoths are increasingly vertically (and horizontally) integrated and could very well continue to outperform in an overheating world. Tomorrow is forecast to be even hotter than today and may well set another heat record in London and the UK more broadly. And given that today was a public holiday, trains and data centers were probably not working as hard as they will be tomorrow. We hope this does not cause disruption. But we wouldn’t be surprised if it did. The State of AI Part 2 - The AI Productivity Landscape - 14 May 2026The enterprise investment case for AI relies fundamentally on the assumption that using AI technologies makes companies more productive. Goldman Sachs points out that consumer adoption of AI has been “spectacular” but that most of those users are accessing a free version, citing a Standford study which found that Generative AI reached ~53% adoption within three years. Covello notes that an “orchestration and deployment layer” needs to be added between enterprises and model developers, that data needs to be structured and deployed properly. This sounds effectively like reducing technical debt - a task which is notoriously laborious and painful for humans, and tends to provide little short-term return (which is why it accrues in the first place). At worst, companies will simply fail to do this and thus ultimately fail to reap the rewards. At best, it will be a rather brutal forensic audit job for whoever is unlucky enough to get tasked with it within the company. Perhaps this is where the Deployment Company (and others) comes in - will they be the ruthless “consultants” brought in to get enterprises more AI-ready? We previously expressed the view that it was more likely that SAAS (and consulting) companies would partner with model developers/hyperscalers rather than be driven entirely out of business by them. Thrive Capital (Joshua Kushner’s fund that is heavily invested in AI) has invested $100 million in Shopify, betting that AI could contribute to gains in commerce; Shopfiy was trading up around 4% later. Given recent examples of unrealised equity gains contributing massively to big tech earnings, it makes even more sense for the AI financial--industrial complex to partner with downstream companies - the mere act of announcing a partnership or investment may be worth the cost of the investment. AI Productivity Research A number of leading research institutions have published research on the impacts of AI on productivity. Published in the QJE Erik Brynjolfsson of Stanford, and others, find customer service agent productivity was improved with generative AI. Erik’s contributions to the field stretch beyond the academic, as the cofounder of Workhelix, which raised $15 million to “better understand and monitor AI automation at their companies”. Another widely cited study was done by the London School of Economics and found that AI saves the equivalent of one workday per week. The report was sponsored by Protivity, a consulting firm that provides audit services. It was formed in 2002 when Robert Half hired over 700 former Arthur Andersen audit employees, the firm which collapsed in the wake of the Enron scandal. Questions for the Future

Hantavirus We’re increasingly following news related to the Andes/Hantavirus outbreak. Given the public health nature thereof it seems unwise to speculate about it, particularly at this stage. However it is promising that transmission “primarily occurs…during prolonged close contact with an infected individual in the prodromal part of the disease”. The Telegraph noted a study today which found that the virus could survive in human sperm for up to 6 years. Could a “parallel pandemic” (a contradiction in terms) or epidemic emerge from this - a situation in which a virus spreads relatively widely across a population but remains confined to certain parts of the population? Given the nature of the transmission, could this suggest that contact tracing may return but be limited to people with whom one has had…”prolonged close contact”? Markets certainly do not seem to be too concerned about this at the moment. Nebius - Another “adjusted net profit” story Nebius reported blockbuster earnings earlier this week and was up over 20% at one point, trading at nearly $220. The major headline figure was probably that revenue had grown from $51 million in 2025 to $400 million in 2026 - nearly 700%. But certainly some of the market reaction must have been due to the gigantic increase in net income. $780 million of net income contribution was made by “gains from revelation of investments in equity securities”. ClickHouse, on of its investments, was valued at $15 billion in a funding round in January 2026. It is possible that, at some point, if the market starts to punish companies that relied on “unrealised gains from equity investments” to pad income statements and earnings per share numbers, that a company like Nebius might suffer for it. Of course, one assumes that Wall Street and the rest of the investor community are wise to these practices. But in this frenzied AI-induced semiconductor rally, what are people really paying attention to? The State of AI Part 1 - Token Maxxing & Goodhart’s Law - 12 May 2026Token maxxing is a “metric used in an attempt to track productivity in the workplace especially for those using Artificial Intelligence” according to Wikipedia. Using this as a metric for productivity is risky for many reasons, one of which is that it might be relatively easy to “game” - that is, to spuriously inflate one’s token usage in order to generate the impression of greater productivity. Hence, token maxxing. It is no irony that the Wiki page also links to “Goodhart’s law” which famously states that “when a measure becomes a target, it ceases to be a good measure”. We decided to look into which companies have been mentioned in the media for pursuing a “token maxxing” strategy. This includes companies that have been “accused” of inflating token usage, and companies that have been noted as using token usage as a metric of some sort, including employee productivity. Our hypothesis is that there are three potential outcomes for companies that do this and as a result for big tech companies that produce AI more broadly:

FT reports that Amazon staff have allegedly been using an “AI tool for unnecessary tasks to inflate usage scores”. Some employees said colleagues were using an in-house tool to automate “additional, unnecessary AI activity to increase their consumption of tokens”. We reference some content from a Reddit post on token maxxing at various companies earlier this week:

They go on to discuss the potential aggregate overestimation of token usage in their post and we concur with some of their logic. It would certainly be insightful if there were an anonymous page where people could report whether this is a more widespread phenomenon than we realise. Perhaps this page could also report on things like how to maximise your token usage. Perhaps we’ll build it next. In other news, the CME is launching a futures market for computing power. It is interesting that the company which Nvidia replaced in the S&P 500, Enron, tried something similar about 25 years ago with “bandwidth trading”. Compute is obviously immensely useful, as was (and is) bandwidth. But perhaps a better, and less fraudulent, execution will make compute power futures trading work where bandwidth trading did not. The infrastructure, at least, is actually in place this time. The Price:Earnings (excl. Investment Income) Ratio for Big Tech - 11 May 2026

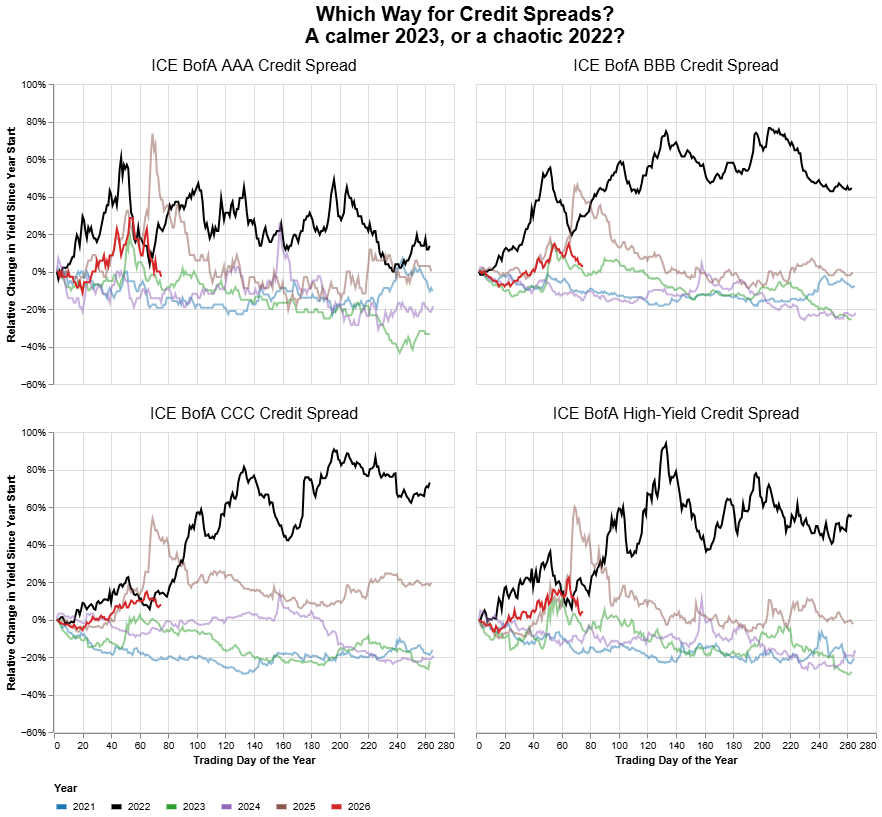

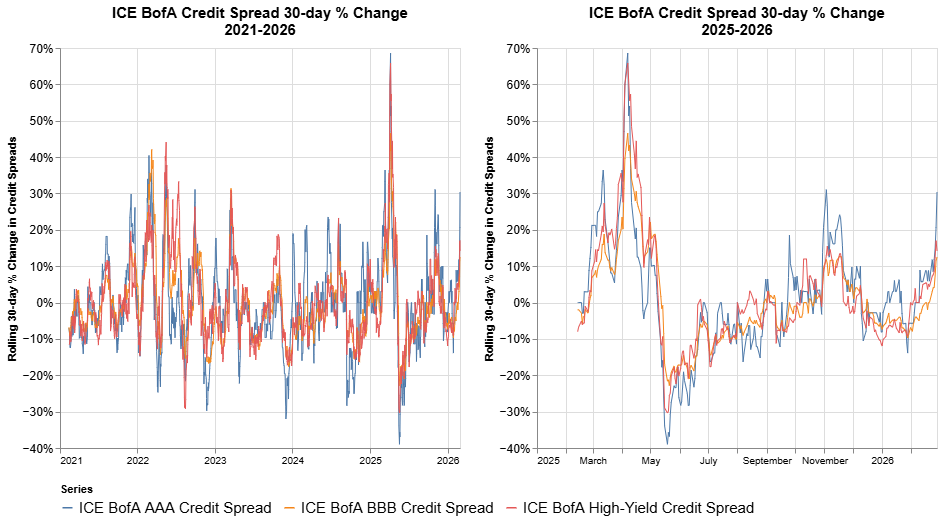

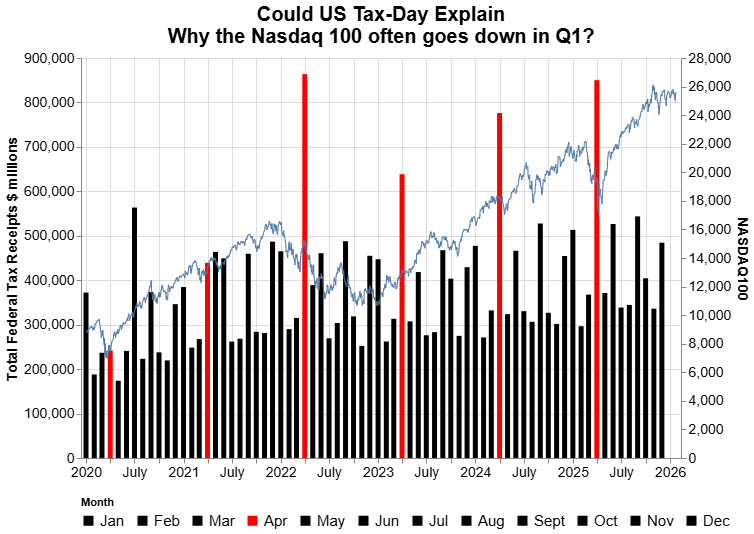

We first noted the phenomenon of big tech companies' earnings being inflated by unrealised gains in their equity holdings in a post on Nvidia and its Intel stake (which, if they have not yet sold it, has continued to explode in value), in late Jan 2026. This “phenomenon” has continued over the last few months, and much coverage has been given to Amazon and Google's recent earnings which were significantly boosted by unrealised gains in the Anthropic stakes. One risk here is of course that the gains from such investing activities may not continue indefinitely. A devil’s advocate would ask - why not? Don’t they already employ the smartest people? Perhaps this calls for other valuation metrics and ratios being used such as those adjusted for income from investment activities instead of the more superficial “earnings per share” or “price:earnings ratio”. Amazon Over a trailing 12-month (TTM) period Amazon’s earnings were around $90 billion at the end of Q1 2026. Adjusting for the ~$28 billion in non-operating income (much of which is due to unrealised gains in its Anthropic stake) puts it at $62 billion. Given ~11 billion in outstanding shares this produces an earnings per share of around $5.6 which puts the price:earnings ratio around at around 50, given a price per share of ~$275. Using the full $90 billion to calculate EPS puts it up nearly 50% closer to $8 and a PE ratio closer to 35. Alphabet For Alphabet a similar story emerges. TTM earnings were around $160 billion by the end of Q1 2026. With around 12 billion shares that produces an EPS of around 13. And with a market cap of around $4.8 trillion this produces a PE ratio of around 30. However when adjusted earnings for “other income” which included nearly $55 billion in unrealised gains on investments, a lower figure of $105 billion in earnings produces an EPS closer to $9 and a PE ratio closer to 45. Where to now? There are some reasons why these blockbuster earnings could continue - the best compensated (and therefore smartest?) people at these big tech companies with enormous balance sheets are now also effectively running large venture capital or hedge funds or each of the LLM companies may maintain sufficient market share and pricing power to transition from their earnings being driven by investment-related activities, to operating activities again. However we think the odds are better that some form of market functioning disruption occurs before then which could distort some of the prices in the AI supply chain and even if not, that this transition from investment to operating income will not be entirely smooth. We are increasingly short but increasingly (however incredulously) open to the possibility that the Trump administration might just pull off keeping this equity market at or near all-time highs into the midterms, with a schedule of potential deals and wins to announce. We will explore various explanations for this soon. For one, the Treasury General Account might have started draining partly due to tariff refunds as Flexport CEO Ryan Petersen reported receiving $137 million in tariff refunds, a source of potentially $10's of billions of liquidity being pumped back into the economy. Tax day taketh, tax day giveth back - 15 April 2026In a somewhat bizarre twist of fate, the Nasdaq 100 is now up 3% on the year, up nearly 15% since the low at the end of March, and closed at an all-time high. This also means that the highly liquid 3x leveraged Nasdaq ETFs like TQQQ are up nearly 50% in 2 weeks. A similarly liquid semiconductor ETF SOXL is up 100%. These are obscene numbers. Credit spreads have come down significantly. It all feels a lot like April 2025 - threats of calamity, a climbdown, and a faceripping rally. This begs the question - where to now? Do we continue to take out new all-time highs, do we chop sideways until the US midterms, or do we begin a descent down similar to 2022? There are quite a few factors to weigh up in the bullish-bearish debate at the moment, which we will do soon. At the moment, we are more inclined toward a 2022 redux. However we wouldn’t put it past the current US administration to send this market to further highs. On tax day We previously highlighted that going into April 15 tax day there would be a liquidity drain which would be positive for the US dollar and negative for risk assets. Of course, the war in Iran played a significant part in this dynamic. The US administration probably took some joy in this year’s selloff of equities that had been bought anytime after the April 7 2025 market lows - these would all have triggered less-than-12-month holding period income tax events. And would also thus be payable in the 2025-2026 tax year. Now that this date has passed, two other forces emerge: 1) for many of the buyers of the April 2025 lows, they are already in the “capital gains tax” 12+ month holding period window, and and taxes payable on these gains are also only due in a year’s time, 2) those same buyers may be holding out hope for an abolition or further reduction of capital gains tax, especially as the next tax day will be after the mid-terms. Credit spreads

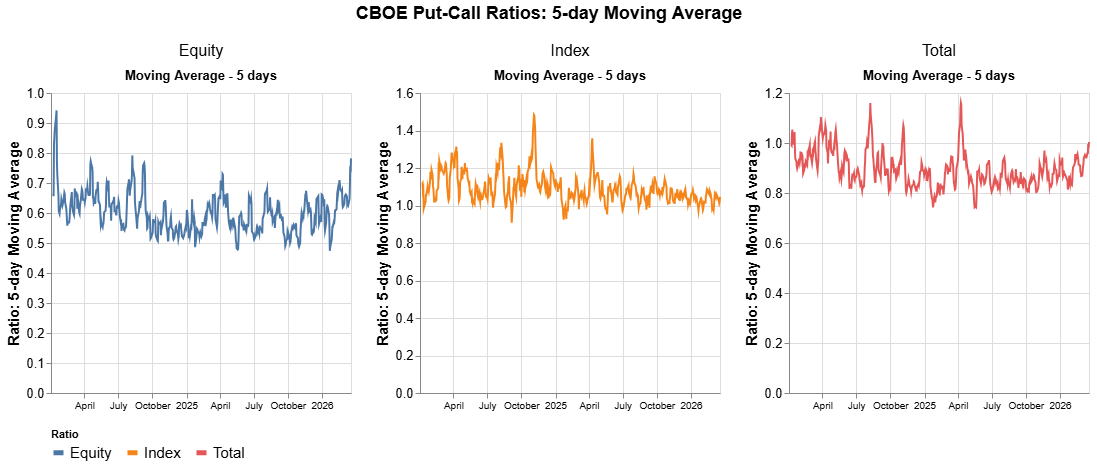

Credit Spread data fromICE BofA via St Louis FRED Credit spreads are down meaningfully. Normally this would signal an easing of liquidity conditions which is positive for risk assets. And there are a number of potential catalysts from the Trump administration, from the Federal Reserve, and from market conditions more generally, which could provide more support. But there is also a problematic parallel with 2022 to consider. CBOE Put-call ratios

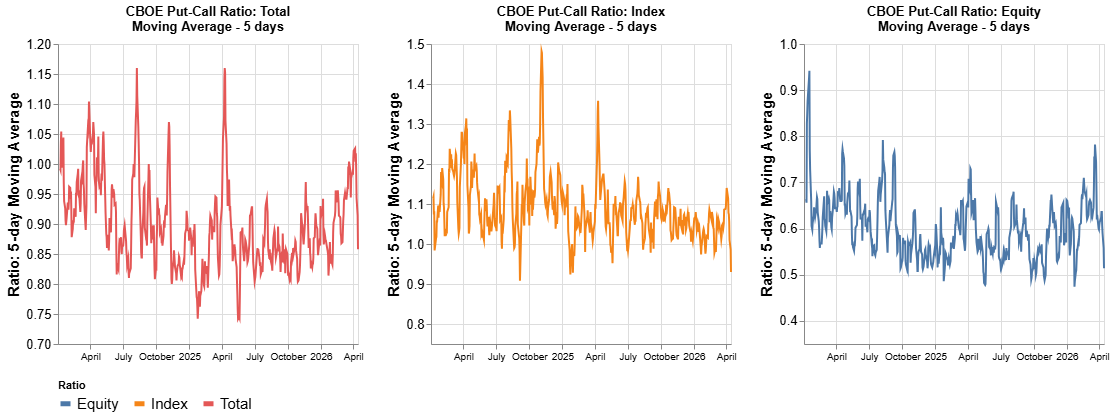

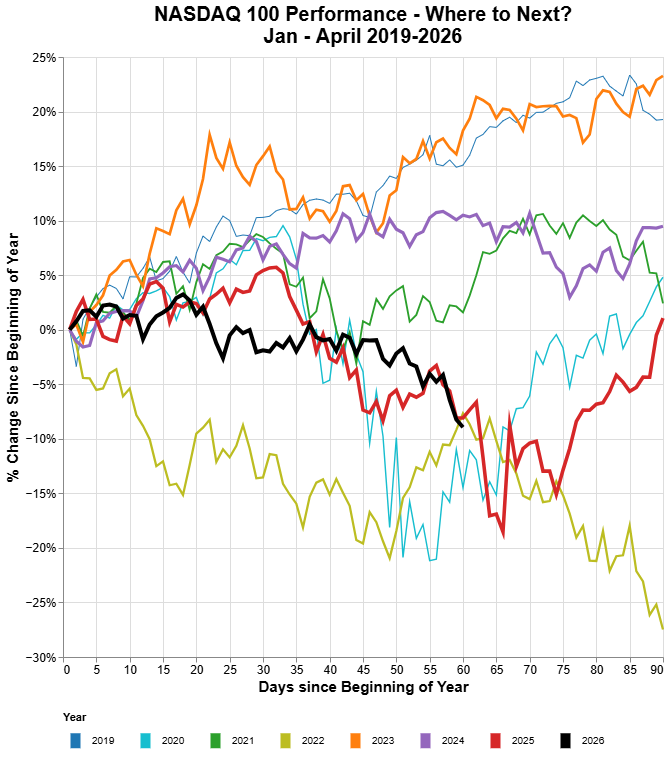

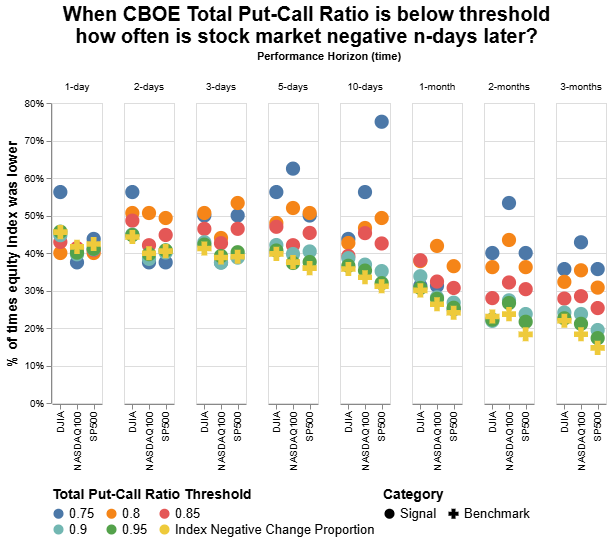

CBOE Put-call ratio data fromCBOE CBOE Put-call ratios have also collapsed. Having previously tested these it seems that sufficiently low PCRs tend to correlate with poor equity index performance in the days after that threshold gets hit. Equity index PCR hit the lowest level in 5 years this past week and the 5-day moving averages are reaching extremely low levels. Potential Short Squeezes or Falling Knife Capital? - 7 April 2026The TACO Trade Strikes Again A 2-week ceasefire, conditional on the Strait of Hormuz reopening, between the US, Israel and Iran was announced today. Oil was down -16% at one point and major US equity indices were up 2-3%. There is an eerie echo in the air in that the market bottomed around the 8th of April last year during the tariff turmoil. The day after that in 2025 S&P 500 gained nearly 10% in a single day. The “relatively” muted 3% gain (albeit after hours) suggests a somewhat more cautious market. European Shorts The FT reported today that hedge funds had made record bets against European companies. Top mention was Wizz Air with nearly 16% of free float short sold. Other companies include British brickmaker Ibstock, shorted by Citadel. The ceasefire announcement today might be enough to spur some unwinding of these shorts. We’re looking at taking a position in Wizz Air, although conscious that any meaningful bump could well be short-lived. Another sector that is starting to look interesting (only because it has crashed so much and because of the headline-driven market we find ourselves in) is UK homebuilders. We’ve been a long-time holder (sadly) initially entering positions during the mid-2022 slump post-Covid work-from-2nd-home boom. The major risk on this front would be that these companies go bust or are acquired at low prices before the cycle turns. The British Stocks and Shares ISA - Some dry powder The new UK tax year started yesterday (Monday 6th of April). What this means is that many people will have contributed as much as they could of their annual £20 000 allowance into their Stocks and Shares ISA (Investment Savings Account). And as a new tax year has started, it means allocations have reset. So it is likely that tens of billions of GBP are sitting in investor accounts, just waiting to be deployed. It remains to be seen whether the ceasefire is a sufficient catalyst for it. Past Results1 Do Not Predict Future Returns(?) - 30 Mar 2026

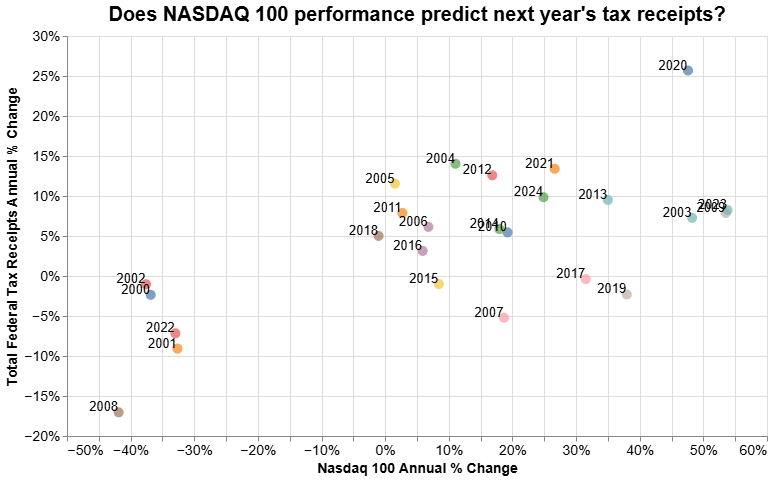

1Stock price data fromYahoo! Finance History may not repeat itself, but it sure does rhyme. The Nasdaq 100 has entered 10% correction territory since its October 2025 peak and is down nearly 9% year-to-date. There is a frantic search for historic parallels to glean what might be next. Is the current macroeconomic situation more akin to the tariff market turmoil in April 2025? Are we seeing a repeat of the 2022 tech drawdown after that bull market peaked in December 2021? Is this another market plumbing meltdown similar to March 2020 (but with geopolitical strife instead of Covid as the looming context)? Or are we seeing a broad-based deleveraging and systemic rupture more similar to the 2007/08 Global Financial Crisis, or a 2001-style dotcom bubble bursting? Tax day approacheth We reiterate the potential “calendar effects” phenomenon we mentioned earlier this year - many funds and individual investors deployed capital in April 2025 in the wake of the tariff market turmoil. Their 1-year/12-month “anniversary” is coming up. It seems likely that there are many investors who will have been spooked into selling by this current market meltdown in order to crystallize solid 12-month return figures. However there is another calculation individual US investors in particular must make - if they sell within a 12-month timeframe the gains will likely be taxed as income, rather than as capital gains. This is potentially a huge difference in return for an investor. Of equal significance is the aggregate potential tax for the US government. US equity markets since April 2025 have gained trillions of dollars in market capitalisation. It is conceivable that if sufficient individual investors who bought securities beginning in April 2025 have been pushed into selling those investments prematurely by the Iran war, the additional tax revenue generated by these sales triggering income tax events (as opposed to capital gains) could number in the tens or even hundreds of billions of US dollars. How many additional tax dollars are generated for each further percentage drop in US equity markets? Does this create a problematic incentive? Fannie Mae and Freddie Mac and Off-Exchange Markets Bill Ackman tweeted over the weekend that Fannie Mae and Freddie Mae federal home loan companies were particularly cheap. Both of these companies were up 50% by the end of the day. In addition to demonstrating again the power of social media platforms in driving sentiment for stocks, this event will likely also drive interest in and awareness of off-exchange securities trading. This fits with our narrative of increased trading on and interest in private capital markets. We have done evaluation of this company however we will assess and potentially invest in OTC Markets Group - the company that provides liquidity and price information for many over-the-counter stocks. Narrative Power - Iran On the topic of moving markets with social media - Iranian parliament speaker Mohammed Bagher Ghalibaf tweeted on Sunday that people should do the opposite of US President Trump’s social media posts seemed to indicate, from an investment perspective. And that pre-market “news” was just a “setup for profit-taking”. This sort of adversarial memetic conduct could have profound implications for financial market integrity. And it probably already has. Has Iran adopted the US playbook of viral diplomacy? Or of financialising conflict? Perhaps Iran is trying their hand at trading oil futures on the back of social media announcements... Long bonds, Circle Internet Drops on Tether - 24 Mar 2026The 30-Year US Treasury Yield The 30-Year US Treasury Bond Yield might be the most important number in international finance. It has bumped up against 5% a number of times in the last 36 hours. And on several of those occasions, and on two in a dramatic way, a news release has sent the yield falling. Most significant was yesterday when President Trump posted on social media about significant progress having been made in talks with Iran. Around 17:50 London time on Tuesday it was reported that the US and a group of regional mediators were discussing the possibility of peace talks with Iran as soon as Wednesday. And then later, very shortly after the close of US cash equities markets at around 20:20 London time, it was reported that Israel was going to announce a 1-month ceasefire. This sent the oil price and bond yields into (brief) freefall and, undoubtedly, wiped out a sea of leveraged short positions. Is the US Treasury conducting yield curve control, through public statements? This time, however, with inflation expectations (at least until the last few weeks) lower than in April 2025, it means that real yields on the 30-year treasury are even higher. Our guess is that this will likely remain a red line for them and so it seems likely that any time the yield approaches that level, one could likely expect some bullish statements from the administration. On the flip side it could very well be that current yields are sufficiently desirable for large and connected investors that we would not be surprised if treasury yields reaching a certain low threshold (around 4.9%) happens to prompt more escalatory headlines out of the administration… A Bad Treasury Auction - but for whom? The US treasury auction this afternoon prompted much discussion as well. A $69 billion auction of two-year notes faced weak demand from investors, and dealers had to step in to take more of the auction. The general consensus seems to be that this is a bad thing. But what if you were a dealer? Bidding for a 2-year treasury at an accepted high yield of 3.936% and then 3 hours later getting to offload it at a yield closer to 3.88%, sounds like a tidy profit. And if one was offloading much of the 20% accepted at that high yield (i.e. around $14 billion), this could mean an extra few million USD just in price-move. Not bad for 3 hours of risk (although admittedly that is forever in the current market). Just a reminder that in this environment, one is paid to hold risk. Let's see what happens at tomorrow and Thursday's auctions. Circle Internet Shares Fall 20% After watching Circle climb another infuriating 20% above our selling price from a few days ago, we watched with the rest of the world as this darling of the last few weeks which had climbed incessantly on days in the face of declines in virtually every other market, including in crypto itself, dropped a horrific 20% in a single day. This was purportedly on news that a draft version of US stablecoin legislation indicated that there would be limits on stablecoin yield. This should not have come as much of a surprise - banks are concerned about losing money to stablecoin issuers, and central bankers are concerned about deposit flight from a stability perspective. The other reason floating around was that Tether has agreed to submit to an audit by a US-based Big 4 audit firm, which it has previously not done. There has been some mystery around Tether’s collateral reserves including what exactly constitutes each particular category. One of the reasons we liked Circle was that it was an “American-made” more transparent stablecoin issuer. If concerns around Tether reserves are founded and they ultimately row back on the more transparent audit, much of Circle’s drop could be reversed. This feels a lot like a headline to fade and had that been the only major crypto news out today, we would have strongly considered re-entering at the current level of $100. Especially given the 4% yields (or more) it will be earning on its many billions of dollars of US Treasuries it holds as collateral. Looking ahead We are confident that if this conflict continues, continued energy disruption and high yields could potentially cause a dramatic contraction in economic activity through demand destruction and potentially elicit intervention by fiscal or monetary authorities that would put downward pressure on yields. The net effect of this, against the backdrop of an AI-fuelled reduction in labour demand, could produce the most dramatic fall in real yields we have seen in a very long time. We feel the global financial system will not tolerate much higher yields, unless they come paired with significantly higher inflation to temper real yields or an extraordinary productivity boost (which today’s data in the US does not suggest is happening…). There is just too much debt maturing soon and governments will struggle to refinance at even current levels, nevermind higher levels. There seem to be only two real outcomes here - much lower yields, not far from now, or a largely unrecognisable financial market. TACOs in Iran - 23 Mar 2026In the minutes before President Trump announced that productive talks with Iran had occurred, which sent the oil price collapsing and equities rallying, there was significant trading activity in S&P 500 and West Texas Intermediate oil futures. This has raised questions around potential insider trading, similar to administration social media posts in April 2025 shortly before a tariff reprieve was announced. Perhaps the less nefarious, but still likely market-integrity damaging, explanation was that it was the administration itself - e.g. the US treasury - that conducted some of these transactions. Either way this reflects a level of risk tolerance from the administration that concerns us - risk tolerance in governments tends to increase when they feel their time is running out. Also, in retrospect, this announcement should have been expected - long term bond yields had reached rather dangerous territory in the morning before. If this turns out to be “fake news” in that it does not represent meaningful progress towards a peaceful resolution of the conflict, we expect significant market turmoil to follow. It would not be the first time that bond market turmoil led to a climb down in negotiations. This, combined with the put-call ratio data we flagged yesterday, as well as positioning data which suggested that many market participants were heavily long oil, were all clues. CBOE Put-Call Ratios1, Fertilisers, and South Korea - 22 Mar 2026

1Put-call ratio data from CBOE South Korea Much has been said recently about the world’s reliance on South Korea (because of the crucial role its two memory giants play in the AI boom) and thereby on South Korea’s reliance on oil, natural gas, and helium imports from the Middle East which supplies a huge amount of these to the country. President Lee has nominated Bank for International Settlements economic adviser and head of research Shin Hyun Song to be the next president of the Bank of Korea. South Korea’s total debt recently reached 6.5 trillion won, marking a record. Government debt to GDP, while not high relative to some other countries, also recently approached a record at 48.6%. Household debt to GDP is near 90% which is second only to Canada’s 100% in the IIF statistics. It will be interesting to see how the new central bank governor steers the Bank of Korea through whatever squall is gathering, with currency pressures, debt pressures, and a potentially catastrophic energy shock on the horizon (not to mention geopolitical pressures…). Perhaps with the government’s relatively low debt ratios, the government could print some debt and it might wind up getting effectively monetised by the Bank of Korea. In early trading the USDKRW breached 1511 to touch the highest level since 2009 and at one point the Kospi was down over 6%. Where’s that swap line? Fertiliser We have a non-trivial allocation to fertiliser companies and have held them for some time. And there seems to be an expectation that the next thing to rally in price could be fertiliser, as a consequence of the Iran conflict. However, fertilizer costs impact food prices and no politician wants that, especially in an election year (even if only mid-terms). It’s one thing to profiteer off of high oil and gas prices, but trying to do so off of fertiliser will likely be catastrophically unpopular. Hence we were not surprised that the US has softened sanctions on fertiliser, and also earlier in the month Bloomberg covered that the DoJ was probing the fertiliser market for potential price fixing. The kicker might be the fact that fertiliser company insiders sold shares quite early on into the start of the Iran conflict, which could suggest that they expect any price uplift to be temporary. We’re still holding, but we would not be surprised if more intervention came to this market. US Equities Market Outlook Total and equity CBOE 5-day moving average put-call ratios have reached their highest levels since April 2025. This has mostly been a contrarian signal - that is, when the put-call ratio is high, and the market is therefore well-hedged against a potential downturn, this often resolves in the opposite direction. This is partly because of vulnerability to short-squeezes - when a sudden positive price movement leads to aggressive buying (short-covering) which causes a positively reinforcing cycle. However much caution is needed here as, at extreme levels, this could also mean that options-sellers are exposed to a sudden downside move. We would not be surprised, however, by a short-term rally in equities here, potentially brought on by positive headlines on Iran. Hyperscalers and PE, UAE Brits Return Home, and South Korean Memory Chips - 17 Mar 2026Hyperscalers (OpenAI) - SAAS - Private Equity Collaboration We recently highlighted that it would make sense for SAAS firms to partner with hyperscalers rather than directly compete with them - partly because if the SAAS/private credit/private equity meltdown continued much further, it could take the broader market down with it, and partly because this way the hyperscalers could have a suitable distribution arm if/when the significant subsidies for LLMs are toned down and they are perhaps too expensive for individual consumer use. OpenAI’s recent announcement about a $10 billion joint venture with private equity to “bolster adoption of its AI software” suggests this is already happening The Great British Remigration UK Foreign Secretary Yvette Cooper indicated today that around 100 000 Britons had flown back to the UK since the start of the Iran war. Around 300 000 Britons are estimated to be in Gulf countries. If the war persists or escalates, we could see a significant portion of these citizens return to the UK. Many of them are holidaymakers but a fair few of them are likely high earners who moved to the UAE for tax purposes. A return to the UK could see many of them reside in places like London which would provide a significant boost to real estate demand. If the escalation is even worse and some of the Middle East becomes uninhabitable, for example because of radioactive contamination through accidental or purposeful nuclear involvement, this could trigger another refugee crisis. And, as it often the case, the wealthiest, most able citizens from there will be the first to leave and set up residence elsewhere. What happens when thousands, perhaps tens of thousands, of relatively wealthy people suddenly enter a city in which construction started on only 6000 new homes in 2025, 94% below the 88 000 per year target? South Korea We’ve been pontificating about the strategic importance of South Korea and its two memory chip giants Samsung and SK Hynix. We noted that Samsung Electronics' chip business CTO Song Jai-Hyuk resigned from the board, after joining the board only a year ago. Recent market gyrations in South Korea after the start of the Iran war has highlighted how sensitive the equity market and possibly the wider economy would be to a spike in the oil price or the US dollar. If the US had any more mercantilist or imperialist designs on this supply chain to secure Pax Silica, but with a stronger hand in it, it has extraordinary tools at its disposal - oil, the US dollar, and the might of the US military, in the event that North Korea’s recent missile launches prove to be more than just a show of force. If anything ever happens to these companies, the only major non-South Korean supplier of memory chips (Micron Technology) would likely perform very well. An interesting pairs-trade to implement this would be to long Micron Technology (which produces about 20% of the world’s memory chips and has its earnings call tomorrow 18th March) and short SK Hynix and/or Samsung. Gilt-y as charged - UK Real Yields1,2 - 16 Mar 2026

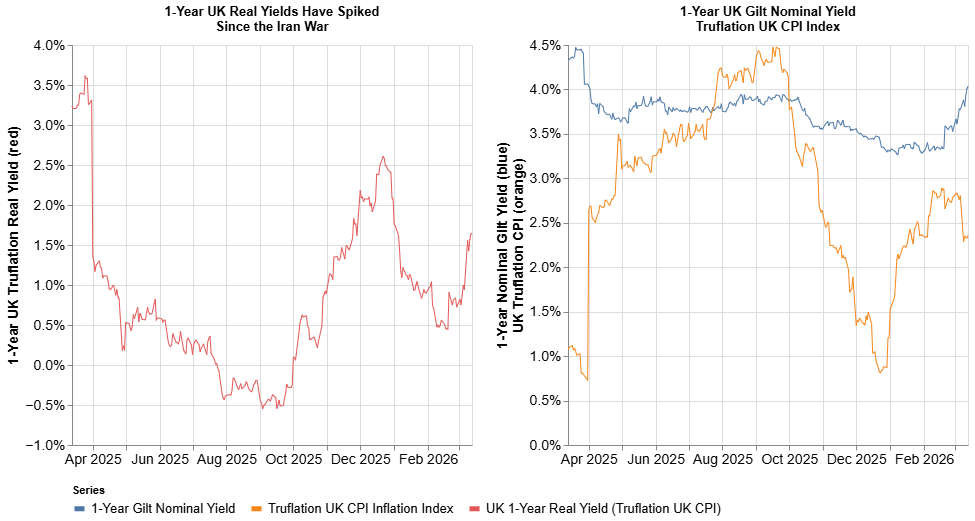

1Bond yield data fromMarketWatch 2UK Inflation data fromTruflation UK 1-Year Real Yields have spiked recently, driven partly by an increase in 1-year Gilt nominal yields and partly by a sudden drop in the UK Truflation CPI Index, and most of this drop was driven by disinflation in Food and Beverages, and deflation in Clothing. This looks to be one of the sharpest increases in UK nominal yields since their ascent from September 2024 to January 2025. Nearly all of the decline in yields since March 2025 has been erased in less than a month. The question arises again whether this spike in real yields is because of tightening liquidity or lending conditions, or whether it reflects expectations for a booming economy. Although retail sales spiked in January, we do not expect this surge in real yields reflects underlying economic strength. Is this time different?1 - 12 Mar 2026

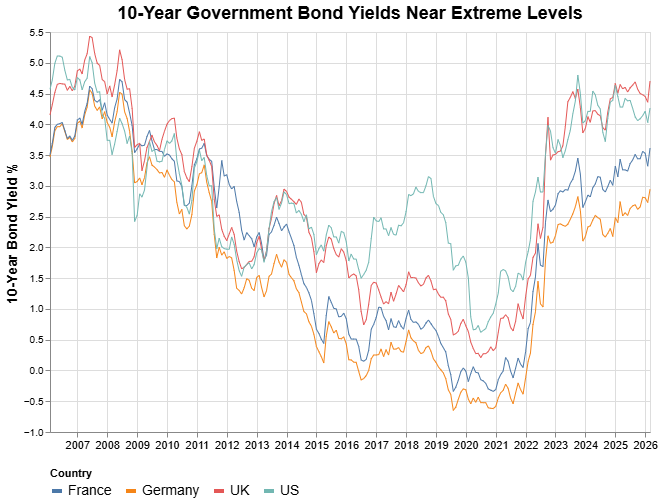

1Bond yield data fromSt Louis FRED Government bond yields have climbed back to recent highs. Credit spreads are at high. The US dollar DXY index is sitting near 100 (October highs). The 10-year - 2-year US Treasury yield spread is at October lows as well. US crude is still comfortably near $95. The USDJPY touched 159.50 yesterday and the USDKRW was back at 1495. Private credit and banking stocks have taken a beating since the start of the year. EURUSD cross-currency basis (a measure of funding stress or USD shortage) has started to flash. And there’s this issue with the war in Iran going on. There are a number of factors which could lead one to believe that something dramatic is going to happen in financial markets, soon. We are certainly close to critical levels which, if breached, could make things get ugly quickly. A couple of contrarian indicators suggests this might not be the case. The VIX has been elevated but indices have not realised commensurate volatility. CBOE Put-Call ratios have spiked higher recently (indicating more puts or downside protection has been bought). Volatility skew on major ETFs like SPY and QQQ is dramatically positive - heading towards April 2025 highs, another indication of more downside protection and that very few are positioned for a “right sided tail” or sudden surge higher in equity indexes. Dealer gamma exposure is negative for SPY which could promote continuation of rallies, and there’s a lot of positive gamma just below current spot levels, which could be counter-cyclical in a selloff. In many ways, the market is primed for a dramatic short squeeze. Any positive headlines on Iran tomorrow or over the weekend and we could see a violent rally. And so for those with narrative power the stage is set to ignite a brilliantly green close for the week. Perhaps a contrarian view to this contrarian view is this - with all this downside protection, and dealers and options sellers having gotten used to absolutely printing money when overly bearish or desperate retail traders have splurged on downside portfolio insurance for much of the last year, are the counterparties truly prepared for a downside move? What happens if there’s a catastrophic headline out of Iran, or a terror incident in a prominent city? Or any other number of potential black swans (we flagged the South-North Korea risk a couple of times in recent months)? What happens if put-sellers blow up, face margin calls, or have to sell other assets (like US treasuries) to fund their positive delta exposure? Of the various scenarios, a dramatic downside event does seem to be the most unlikely (based on the doctrine of “nothing ever happens”). But in our view, it is precisely because it seems so unlikely, because there is so much downside protection out there, that its risk might still be underpriced. There was also something else that caught our attention today. The CME Group chair Terry Duffy warned that the US government risked disaster if it intervened in the oil market via derivatives trading, as people could lose confidence in the market’s capacity to price commodities correctly. The article suggests there has been much speculation about the US government possibly being responsible for the large transactions over the last few days, giving some credence to our thinking that the US might be increasingly behaving like a large trader. One reason this caught our attention is that doing so seems incredibly risky in a number of ways, and would reflect in our view a dramatic shift in the Trump administration’s position, as well as a shift in risk tolerance. And risk tolerance tends to go up when you sense your time is running out or you expect some dramatic event in the near future. We still think the most likely path would follow the “nothing ever happens” route - relevant indexes and commodities would oscillate between key levels, not triggering any dramatic in-the-moneyness for either calls or puts, which would therefore expire worthless and options sellers would collect the vast mountains of premium that the market has been willing to pay this past couple of weeks. This would likely be paired with impactful headlines appearing near key price levels, pushing the relevant security away from that level. We saw a lot of this yesterday, with dollar-negative headlines smashing the DXY down repeatedly from around the 99 level (which, incidentally, in the absence of any such headlines it continuously reclaimed). The second most likely scenario is for a fair bit of upside, triggering some amount of a short squeeze and pushing major indexes into positive gamma exposure territory for dealers. And finally, a significantly negative market move tomorrow could prove disastrous if the magnitude was significant enough, as we don’t think bonds could take much more selling off before they triggered more systemic concerns. Narrative Power1,2 - 11 Mar 2026

1US Oil price data fromMassive 2News headline data fromMKTNews Narrative power is the ability of stories, myths, and shape framing to shape reality and influence beliefs. In modern financial markets, it manifests in the ability of influential people to move markets with their words. President Trump did so famously in April 2025 when tweets around tariffs sent global financial markets reeling, and markets rallied after he wrote on Truth Social that investors should buy stocks. Last night narrative power rested with US energy secretary Chris Wright when he tweeted that the US had escorted a tanker through the Strait of Hormuz. Shortly after, oil prices plunged (shown above by the price of the US Oil ETF) and then rebounded after he deleted the tweet. Given the recent volumes in that and other oil ETFs, that move in the oil prices likely obliterated some leveraged positions and inflicted extraordinary losses (and gains) on holders. Oil Reserves Several countries including the US indicated today that they would deploy significant reserves from their strategic petroleum reserves. But it soon became clear that a specific timeline was not immediately available. For the US it would take approximately 120 days to fully deliver the Energy Department’s reserve. We would not be surprised if this and other actual deployment only started to occur at higher oil price levels than current, especially when looking through the lens of sovereign or “nation state" traders. Trader States And speaking of nation state traders, the Pentagon is allegedly recruiting from top tier investment banks for an “Economic Defense Unit” with the stated aim of “helping deter our largest adversary from gaining military superiority”. It seems President Trump’s dreams of a sovereign wealth fund are manifesting, in various forms. Given the amount of US debt maturing this year and the recent spike in credit spreads and US treasury rates of various tenors, perhaps the US is looking to not only secure critical minerals, but might be attempting to trade its way out of a fiscal deficit. The combination of the most powerful military, extraordinary narrative power, and a near-limitless balance sheet, surely would make for the most incredible hedge fund. It is worth remembering that US Treasury Secretary Scott Bessent was a partner at Soros Fund Management and is (probably) a trader in his bones. Other News: Section 301, THAADs in South Korea, Circle In “stories which we think may begin to dominate the narrative after Iran”, we highlight that the US is launching an unfair trade probe into 16 countries. Also, as the US has removed some of its THAAD batteries from South Korea to deploy them to the Middle East, we wonder whether this might spur North Korean aggression and posturing in the near future. There’s a huge amount of market capitalisation contained in the Kospi now, and the US would likely not look fondly on its flow of memory chips being disrupted. Definitely one to watch out for. Finally, we closed our Circle Internet Group Position today for a total gain of 50%. As per the usual contra-indicator this may well mean that most of its growth is yet to come. But the price action today looked a bit strange - with a gap to $122 on the open and declining to a low of around $113. We are still pro agentic commerce, stablecoins and the adoption thereof in general, as well as Circle in particular. We may re-evaluate and re-enter at a later stage, at a lower or even at a higher price. Neo-imperialism or just Neo-mercantilism? - 9 Mar 2026In a bizarre case of deja-vu, US equity indices finished the day higher on Monday than they closed on Friday, following a dramatic decline after Sunday night futures open. This follows an eerily similar pattern to Monday the 2nd of March after the first weekend’s strikes of Operation Epic Fury. Another episode of “Nothing Ever Happens” characterised by significant intraday and intra-index volatility but very little change in the index itself. A passive investor would barely have noticed. Oil positioning and flows - don’t get caught holding the bag It is becoming something of a trope that “retail investors” come into rallies near the end and are often left “holding the bag”. This might have been the case again as retail investors piled $82 million into the United States oil ETF USO. A huge proportion of this ($36 million or 42%) was done on Friday alone. This beats the 5-day record of $67 million in 2020 when oil price briefly turned negative during the Covid crash. Precious metals and equity ETFs saw significant outflows whereas energy ETFs saw extraordinary inflows. Oil did indeed spike as the conflict with Iran escalated dramatically over the weekend, with US and Brent crude oil trading up nearly 30%, towards $110 per barrel, triggering a restrike event for some leveraged ETFs. This brings the number of commodities underlying ETFs that have experienced restrike events this year to 3 (oil, natural gas, and silver), which we suspected would happen again. Given that oil proceeded to collapse from the day’s high around $115 to a low of $83 (-28%), and that many retail traders often access commodities and related funds with leverage, it is probably safe to assume that many of their trades were wiped out. Parsing current signals and rhetoric around the conflict is difficult, with some indications today that the conflict could be over soon. However there are still a few disruptions or escalatory events which we have not seen, which may yet come to pass - damage to AI datacenters in the UAE, potential radiation leakage from bombed nuclear sites, cyber incidents, or more severe aggression towards vessels trying to transit Hormuz.Any of these could be a trigger for another bout of volatility in equities and oil prices. Trader USA 2026 so far is showing that the Trump administration might be steering the US into not just a neo-mercantilist direction, but also into a neo-imperialist one. One of the themes we see emerging is that of “USA the trader” - that is, the US government more actively participating in markets. The markets that the US government has participated in so far include listed equity markets (e.g. MP Materials, Intel), private markets (Atlantic Alumina), strategic metals and rare earths (Export Import Bank loan to establish Project Vault), cryptocurrency (the crypto strategic reserve) One could add the strikes on Venezuela, which has vast oil and natural gas reserves the US can exploit, Iran and potentially Cuba as well soon (which has significant cobalt and nickel reserves). For the most part, these examples see the US government as a buyer (and a lender in the case of Project Vault). The latest addition to this phenomenon sees the US as a seller, in the shape of the Development Finance Corporation’s deployment of Maritime Reinsurance to secure up to $20 billion worth of losses. It will be interesting to see which “best in class” preferred American reinsurance partners will participate in the endeavour, and how the reinsurance backstop will be implemented. Fun fact: the current CEO of the DFC is Benjamin Black, son of financier and Apollo founder Leon Black, and was also previously a senior portfolio manager at Knowledge Universe (founded by “junk bond king” Michael Milken). Pax Silica - South Korea If Pax Silica provides any indication as to the priorities of the US government (in terms of resource acquisition) ensuring the continued supply of microchips (GPUs from Taiwan or memory chips from South Korea) likely ranks very highly on that list. Blackrock Financial Advisors already owns 5% stakes in both Samsung and SK Hynix. It would not surprise us to see US firms taking further stakes in this supply chain. But whether it occurs soon and near the current all-time highs of the Kospi, or later at more distressed levels, perhaps when a USD:KRW swap facility becomes necessary again, will give us some clues as to the intentions of the administration. There might have been some interim relief in the dollar shortage in Korea as the Swiss National Bank recently renewed the 10 billion CHF swap facility with the Bank of Korea, and it might be easier to turn CHF into USD. Weaponising the US dollar to secure a supply of components necessary for AI would certainly be a novel exercise… We wonder whether this practice will continue to characterise 2026 and the remainder of President Trump’s tenure - using the fiscal and military might of the US government for more active and aggressive resource acquisition. We suspect that this will almost certainly be the case. Private Credit, SAAS and those who wish to disrupt them SAAS has a near zero marginal cost, subscription windows that last some time, and in many cases produce products that many end-user companies would probably not want to insource or take responsibility for, and which hyperscalers and FAANGs may not want to develop robust versions of (e.g. HR platforms and possibly also CRM). We think it would be more likely for hyperscalers to ink deals with the SAAS companies whose share prices they have disrupted in recent months. Another important factor is that if the SAAS disruption continues for much longer, private credit’s downturn may deepen which could have knockon effects for credit spreads, employment and the wider economy. There is a real risk that a deep enough downturn could spread to other systemic financial market participants like insurers. If that happens, the wider equity market could very well follow. SAAS will become customers, rather than competitors, we feel. Private credit firms also likely do not want the SAAS downturn to continue, for the same reasons. But in addition to that, private credit lenders also do not necessarily all want to end up owning and operating the companies that they have lent to (which is increasingly the case, and looks set to continue). For those that have, and will, it would likely also make sense to (in addition to the relevant streamlining/efficiencies commensurate with such a takeover) engage with hyperscalers in a collaborative way, rather than a directly competitive way. On this superficial level, it makes sense for collaboration rather than disruption into oblivion to be the theme of the SAAS-hyperscaler relationship, which could suggest short and/or long term recovery in SAAS equity. There are crucial caveats to this however - it makes no explicit claims about the fundamental valuations, which many people (including Cliff Asness) seem to have questions about. The March-April Macro context We don’t generally give much weight to simple calendar effects in markets. But there are a few things happening over the next month or so which could have significant market impacts.

There is another somewhat vague calendar effect coming up soon as well. The 1-year anniversary of when the US equity market bottomed on the 8th of April 2025 is coming up. And while that itself is irrelevant, it does mean that any fund or investor that deployed capital during the downturn or in the early part of the recovery, will be setting their 12-month “performance” metrics soon, as well as potentially seeking to lock in the gain (which in e.g. the Nasdaq 100 has been an extraordinary ~50%). This could create further selling pressure. And given that the US has an extraordinary amount of debt maturing in 2026, and may have to refund $150 billion in tariffs soon, perhaps the IRS wouldn’t mind a bit of a selloff to act as the impetus for people to lock in their taxable gains, much of which might fall inside the 12-month holding window and thus be taxed at much higher rates. The Trump-Xi summit in early April is also well timed to be a potential catalyst for a market recovery, in the same way that the tariff de-escalation was a catalyst for the 2025 monster rally, if we continue lower from here first. More significant volatility ahead seems to be something of a foregone conclusion, with many potential sources of headline and event risk. The Kimchi Premium in South Korean Equities1 - 4 Mar 2026

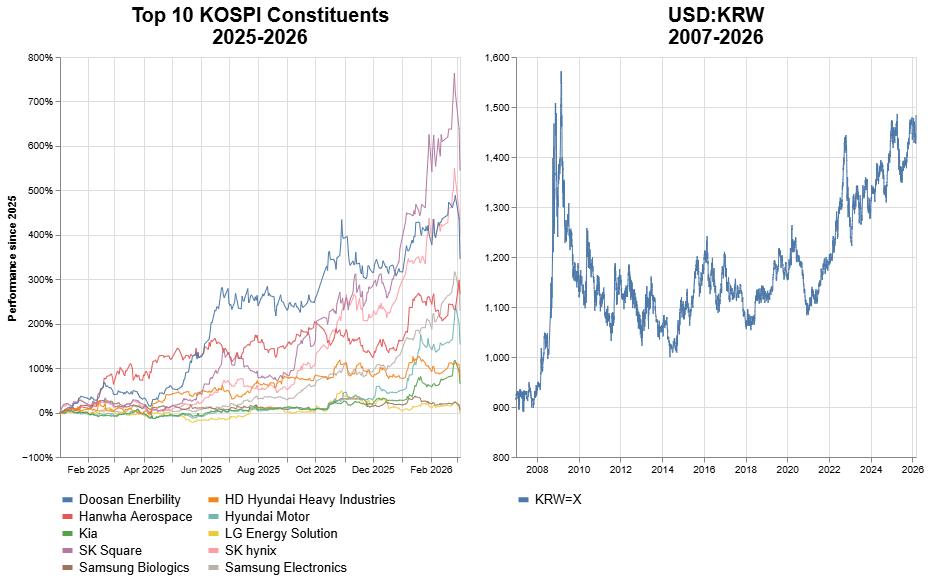

1Stock price data fromYahoo! Finance Kospi and USD:KRW Extreme Moves The South Korean Kospi equity index saw its worst day in history, falling 12% and triggering two circuit breakers. After which in the early hours of the morning, it hit limit-up again and triggered another circuit breaker. The USDKRW rate briefly touched 1510 last night before weakening back towards 1460. This level was the highest since the 2008 Global Financial Crisis. This and the Kospi’s recent performance are reminiscent of the USDJPY hitting 160 just before the Nikkei had its largest drop since 1987, in August 2024. If the parallel with Japan is to continue, this could mean some sideways trading for the Kospi from here on. It is also notable that the USDKRW dipped significantly after hitting the 1500 level the first time, before it hit a new high in 2009 around the time US stocks bottomed. While much of the gains in these stocks is undoubtedly explained by surging demand, it is worth remembering that the economy contracted somewhat in Q4 2025 and has previously led other economies. Kospi Leaders Although South Korean companies like Samsung and SK Hynix have been major beneficiaries of the AI spending boom, particularly due to increased memory costs, it seems the biggest gainer since 2025 has been SK Square which is, amongst others, the holding company of SK Hynix and part of SK Group the 2nd largest conglomerate in South Korea. Fun fact, according to Wikipedia the CEO and Chairman of SK Group is Chey Tae-won, who was previously married to the daughter of former South Korean president Roh Tae-woo, and was found guilty of embezzling $40 million to cover up his trading losses and sentenced to 4 years in prison. The current president, Lee Jae Myung, who has been indicted various times, was once a day trader himself and has prioritised boosting the South Korean stock market. USD:KRW Swap Lines In October 2025 South Korea and the US were discussing setting up a bilateral exchange swap agreement, so that its currency markets would not be skewed by the proposed $350 billion South Korea had promised to invest in the US as part of a trade deal. Supporting this deal will be put to a vote on March 12. The South Korean minister for economy and finance Koo Yun-cheol indicated that the US had rejected a cross-currency swap, as South Korea reportedly held nearly $1 trillion in foreign reserves. Perhaps part of the reason for denying this swap line was that it would signal crisis conditions, or weaken US leverage against South Korea in enforcing a trade deal. Or perhaps the US wants to become an exporter of memory chips through Micron. Given that President Lee has recently indicated the FX and stock market volatility need to decrease, it will be interesting to see how this needle is threaded - USDKRW is at near-record highs, the Kospi recently had its worst day ever (and is still up significantly year-to-date), they need to start making investments into the US, and may need to use US dollar reserves to intervene in their currency markets. DeFi, Real Rates, Private Credit1, Iran - 3 Mar 2026